Unless there is more information not available in the public record, former Federal Reserve Governor Lisa Cook appears to continue to benefit from allegedly lying on her mortgage loan applications. When the automatic drafts hit Cook’s account next month for her two mortgages, she will continue to profit from having claimed to live in two different houses on two different loan applications. In other words, if Cook did commit mortgage fraud, the crime is still in progress.

Cook has now filed a lawsuit in the D.C. District Court challenging the legality of President Trump’s for-cause termination of her tenure as a Fed governor. Her lawsuit argues that the allegations against her are “unsubstantiated.” That’s a dubious claim for her to make. Her own lawsuit contains the substantiation in Exhibit A, part of which is shown here:

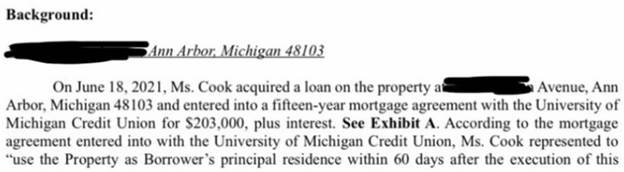

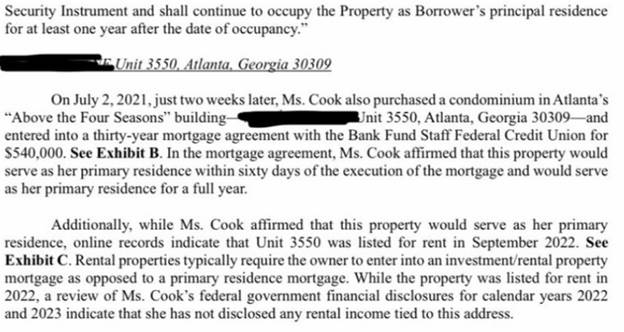

Note that the text states that Cook, in the space of two weeks during 2022, claimed two different homes as her main residence; the government alleges that she did this in order to obtain better loan terms. Banks charge a lower interest rate for an owner-occupied primary residence because, should a borrower come under financial distress, lenders assume the borrower will default on an occupied home loan last.

Cook was a public official acting in one of the most important bank supervision roles in all of government. She has been credibly accused, and has not denied, signing two different loan agreements in which she claimed to be entitled to a lower interest rate.

Cook’s lawsuit claims that these mortgage loan documents are old news and are all in relation to things that happened before she became a governor. On the contrary, unless circumstances have changed—and there’s no evidence in the public record that they have—Cook is still paying the lower rate and continues to benefit from the misrepresentations she made on loan documents in 2022. Again, if this is mortgage fraud—and Cook is entitled to the presumption of innocence—then the crime is still in progress.

To correct this alleged fraud, Cook would need to repay at least one of these loans and repay all of the interest savings she obtained from the misrepresentation. There is no indication she’s done this; instead, she is attempting to force the president to retain her as a Federal Reserve governor even while continuing in this alleged fraud against two different credit unions.

Cook’s lawsuit also claims that she’s entitled to a judicial hearing before the president can fire her. That’s not how it works. The president, not a judge, has the power to fire public officials. A judge has the power to reverse that decision with cause, not to make it in the first instance.

The president’s critics have also complained that Cook’s privacy rights have been violated by the public airing of her private loan documents. If Cook were some low-level federal employee, they may have a point. But her duties as a Federal Reserve governor require public confidence in her integrity. If she’s committing mortgage fraud (and again, she’s entitled to the presumption of innocence) then the public interest outweighs her right to privacy. Her integrity is a matter of public concern. The Trump administration’s transparency on the issue is consistent with that principle.

Unlike the many criminal accusations against Donald Trump, in which clever prosecutors stretched the law to invent novel justifications for charging him with a crime, this is a real crime for which many real Americans have been convicted. For example, in December of last year, a federal jury convicted Kevin Smith, a real estate professional, of five counts of originating loans for 14 properties during which he caused the borrowers to misrepresent their intent to occupy those properties as primary residences. In 2012, the U.S. Attorney for the Eastern District of Virginia obtained convictions against five individuals for mortgage fraud. “The fraudulent mortgage loan applications contained false information regarding the applicant’s employment, income, assets, immigration status,and intent to live in the property as a primary residence.”

Was the firing of Cook politically motivated? Of course it was. But so was her appointment.

Cook is an openly partisan social justice advocate who promised to use her position to further her racial justice aims. The fact that the current president also has political and policy reasons for the removal does not give her immunity to continue committing mortgage fraud. How would the press react if President Biden had fired a Trump appointee credibly accused of the same thing? The question answers itself.

Cook is certainly entitled to remain silent in the face of these allegations. But she is one of the highest-ranking public officials in the country and she has a heightened duty to maintain the public’s confidence in her integrity. If she cannot provide a plausible rebuttal, she cannot continue to expect the president’s confidence in her ability to perform her duties. She should have resigned her position if she was not prepared to provide an explanation demonstrating her innocence. Absent a resignation or a reasonable explanation, the president cannot be expected to look the other way. It’s Cook’s fault, not the president’s, that it has come to this.

Leave a Reply